Almaden Minerals' $1.06 Billion ICSID Claim Against Mexico

Bonus Content: An update on Panthera and other interesting ICSID litigations

Before getting into the main topic of this article, I would like to begin with a brief update on Panthera (PAT:LSE) along with an introduction to another case called Equatorial Resources (EQX:ASX).

Both of these topics are covered in-depth by Swen Lorenz of Undervalued Shares.

If you like the type of things I write about, you should definitely subscribe to his newsletter and read his latest article which covers Equatorial Resources (in depth) along with a detailed update on Panthera and other interesting ICSID Litigations.

Panthera, which was originally written up by Swen, has already returned over 100% since publication. The case is reaching a critical stage, when the SOC will be filed, and we find out how much money the company is litigating over. Panthera is my highest conviction ICSID play at the moment, given the counterparty, the sizable gold concession in dispute, and the facts of the case.

The other two sovereign litigations that sit right behind Panthera, in my view, are Almaden Minerals (covered below) and Equatorial Resources.

In short, Equatorial has a close to 2 billion dollar claim. It trades at almost cash value, with no debt and few stock options. There is no litigation funder to sop up any settlement. The country involved failed to show up to defend itself at its hearing. In fact, it didn’t even pay its lawyers! It reminds me a lot of the recent successful Tanzania litigation cases. Read Swen’s article to learn more.

With that said, onto Almaden Minerals, which I consider the most interesting litigation going on in Mexico.

Almaden Minerals' and its claim

In March 2025, Almaden Minerals made headlines by filing memorial documentation for a substantial US$1.06 billion damages claim against Mexico under the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), one of the largest current claims in the ongoing wave of litigation against Mexico.

This article examines Almaden's claim in detail, but first, before that information on Mexico and ICSID litigations.

Mexico is the third most sued country in Latin America and the Caribbean and the fourth globally with the majority of the claims in the mining and oil and gas sector with over 55 cases.

Mexico is a relative newcomer to ICSID, joining only in mid-2018. The intention was to prove it would honor legal agreements with foreign investors even if the government changed.

In reality, Mexico has a terrible history of honoring agreements with multiple nationalizations of foreign investor assets. It has been sued every single year since the ICSID agreement was put into place. Almaden seems to be one of the most likely cases to succeed.

Almaden Minerals' Billion-Dollar Claim: Background and Context

Almaden Minerals Ltd. (TSX: AMM; OTCQB: AAUAF), together with Almadex Minerals Ltd., has initiated international arbitration proceedings against Mexico through the International Centre for Settlement of Investment Disputes (ICSID).

The dispute centers on the Ixtaca precious metals project located in Puebla State, Mexico—a significant deposit with proven and probable reserves of 85,159,000 ounces of silver and 1,387,000 ounces of gold

The roots of this dispute trace back to 2015 when an ejido community declared itself Indigenous and filed a lawsuit challenging Mexico's mineral title system.

Despite Almaden's attempts to relinquish 7,000 hectares including the ejido lands, the situation escalated under President Lopez-Obrador's administration.

In 2022, Mexico's Supreme Court ordered the suspension of Almaden's mineral titles pending Indigenous consultation, but in 2023, Mexico's mining authority (Economia) denied the company's mineral title applications retroactively, citing minor technical faults

The formal dispute resolution process began in December 2023 when Almaden delivered a Request for Consultations to Mexico under the CPTPP.

After a consultation meeting on May 30, 2024, failed to resolve the dispute, the company filed notice of its intention to submit a claim to arbitration on March 14, 2024.

The official Request for Arbitration was filed with ICSID on June 17, 2024.

The Basis of Almaden's Claim

Almaden's memorial submission outlines three primary allegations against Mexico:

Unlawful expropriation of the claimants' protected investments without compensation

Failure to accord fair and equitable treatment to the claimants' investments

Unlawful discrimination against the claimants and their protected investments

The claim is being financed by up to US$9.5 million in non-recourse litigation funding provided by a leading legal finance counterparty.

Boies Schiller, a successful international arbitration firm, that has won in a number of arbitration disputes, notably and most recently with three Tanzanian Litigations (Indiana Resources, Montero, Winshear) is representing the claimant.

Based on an independent quantum expert's valuation, the claimants are seeking damages of US$1.06 billion—a figure that may be updated as the claim proceeds to reflect movements in precious metal prices, exchange rates, and other factors. As we all know, Gold and Silver prices are going up daily.

Relationship between Almaden and Almadex

Almadex (not to be confused with Almaden) is a co-claimant in the ICSID arbitration alongside Almaden. While Almaden was the owner of the Ixtaca project, Almadex’s interest derives from its 2.0% NSR royalty on the project. Both companies, together with their Mexican subsidiaries, are pursuing claims for damages resulting from the loss of their investments.

To streamline the arbitration process, Almaden and Almadex entered into a Litigation Management Agreement. Under this agreement:

Almaden bears the up-front costs of the arbitration and provides overall direction for the proceedings for both itself and Almadex (and their subsidiaries), with some limitations.

Almadex remains a party to the arbitration, cooperating and supporting the process, but does not manage or fund the claim directly.

If damages are awarded, Almadex will receive a pro rata portion corresponding to its royalty interest, minus its share of costs and financing expenses. Almadex will pay Almaden 10% of its award as compensation for managing the claims

Given this relatively small royalty, it is doubtful Almadex will receive very much of this claim.

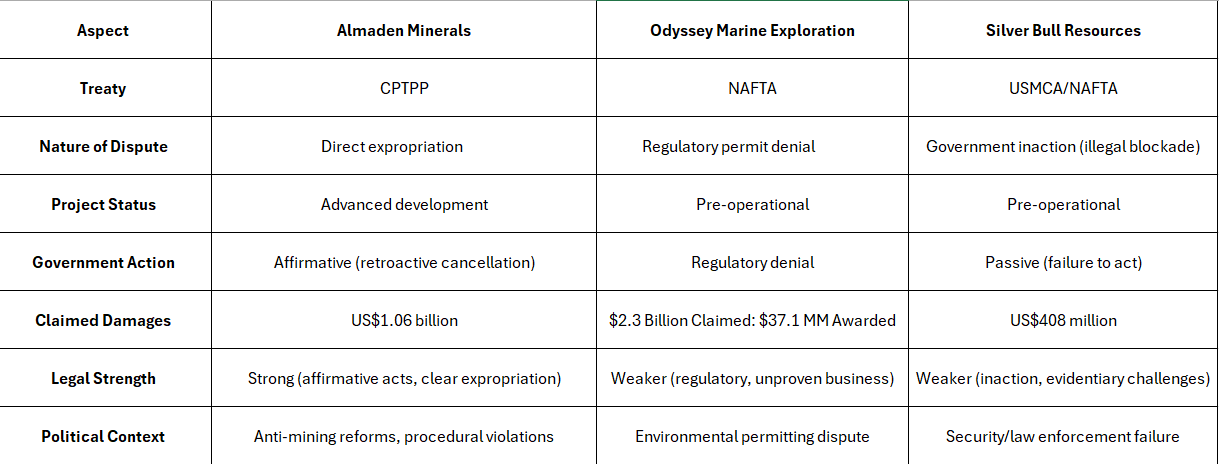

Comparison of Almaden’s Claim vs Silver Bull/Odyssey Marine

The arbitration cases of Almaden Minerals, Silver Bull Resources, and Odyssey Marine Exploration against Mexico offer a revealing look at the evolving risks and legal frameworks facing mining companies in the country. While these cases are often discussed together due to their high profiles and similar sectors, their legal merits and factual circumstances differ significantly.

Almaden Minerals: Direct Expropriation and Political Interference

Almaden’s US$1.06 billion claim under the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) stands out for its clear focus on direct government expropriation. The company alleges that Mexico retroactively canceled its mineral titles for the Ixtaca project following a Supreme Court order for Indigenous consultation, despite Almaden’s efforts to comply and relinquish disputed lands. The situation escalated under President López Obrador’s administration, which had adopted increasingly anti-mining policies, including a refusal to issue new concessions and reforms that have unsettled investor confidence Almaden claims that these actions amount to an unlawful taking of its investment, compounded by procedural violations and discrimination, with the project already at an advanced development stage.

Odyssey Marine Exploration: Regulatory Denial, Limited Damages

Odyssey Marine’s arbitration under NAFTA resulted in a US$37.1 million award—only about 1.5% of its original claim. While this may seem discouraging, the facts of the Odyssey Marine case have little bearing on Almaden.

The dispute centered on Mexico’s environmental agency denying a permit for Odyssey’s early-stage, speculative, offshore phosphate mining project, rather than on outright expropriation. This regulatory dispute, lacking the element of affirmative state seizure, was viewed less favorably by the tribunal, resulting in a much lower award.

In short, Odyssey’s project was not only technologically ambitious but also highly experimental; it proposed extracting phosphate from the ocean floor using methods that had never been deployed in scale anywhere in the world.

Seabed mining has never been found, to date, to be commercially viable for mineral extraction (as much hype as it gets), and there is not a single business in the world currently mining this way in any meaningful capacity.

This lack of precedent made the project inherently risky, with significant technical, environmental, and regulatory uncertainties and difficult to apply a net present value to. The company had invested heavily in environmental studies and secured a long-term concession, but it remained pre-revenue and dependent on external funding along with an unproven concept.

The denial of a crucial environmental permit by Mexico’s regulatory agency-later found to be politically motivated-became the focal point of the dispute, but the tribunal ultimately saw this as a regulatory issue with indeterminate damages from a speculative project.

The tribunal’s decision to grant only a fraction of Odyssey’s claimed losses underscores the broader difficulties in quantifying damages for projects in industries that are still in their infancy and have yet to prove commercial viability.

Seabed mining, as envisioned by Odyssey, remains a non-commercial activity globally, largely due to unresolved technical challenges and the absence of established regulatory frameworks.

Environmental concerns, particularly in ecologically sensitive areas, further complicate the path to commercialization, as governments are understandably cautious about permitting activities with unknown risks to marine life and local economies.

In this context, the arbitration outcome reflected the risk profile of the business: while acknowledging Mexico’s improper regulatory conduct, the tribunal discounted Odyssey’s projected future earnings as highly speculative, given the project’s early stage and unproven methods.

Silver Bull Resources: Inaction and Evidentiary Challenges

Silver Bull’s US$408 million claim, under the USMCA/NAFTA, is based on Mexico’s alleged failure to act against a five-year illegal blockade at its Sierra Mojada project.

The company argues that Mexico’s inaction constitutes expropriation and a denial of fair and equitable treatment. However, the claim hinges on proving that government inaction—rather than affirmative state measures—led to the loss of investment, a position that typically faces higher evidentiary hurdles in arbitration.

Silver Bull’s claim also involves a pre-operational project and lacks the clear-cut procedural violations seen in Almaden’s case.

An update on their process can be found here.

Comparison Table of Three Claims

Analysis

While it is tempting to draw direct parallels between these cases, the legal and factual distinctions are critical. Almaden’s claim is strengthened by clear, affirmative government actions that amount to expropriation and are accompanied by procedural irregularities—factors that tribunals have historically viewed more favorably than regulatory disputes or failures to act. The use of newer treaty language under the CPTPP, which may provide stronger investor protections, further distinguishes Almaden’s case from Odyssey’s, which relied on older NAFTA standards.

Odyssey’s disappointing result reflected tribunal skepticism toward regulatory disputes, especially when the project is not yet operational, highly speculative, and there is no direct evidence of expropriation.

Silver Bull’s claim, while similar in some respects to Almaden, faces the challenge of proving that government inaction in the face of third-party interference constitutes a treaty breach—a higher bar to clear in arbitration.

Conclusion

Almaden Minerals' US$1.06 billion ICSID claim against Mexico underscores the growing risks faced by foreign investors in Mexico’s mining sector amid shifting political and regulatory landscapes.

Unlike previous cases such as Odyssey Marine, which centered on regulatory permit denials in an unproven business model, Almaden’s claim is grounded in direct expropriation through the retroactive cancellation of mineral titles and clear evidence of political interference.

The outcome of Almaden’s claim will likely set an important precedent for both investors and the Mexican government, influencing future disputes and the broader landscape of investment arbitration in Mexico.

Finally, keep in mind the stock’s current market cap is ~$14 million as compared to a $1.06+ Billion claim, and that the litigation is fully funded through a third party, so the risk-reward on this one is high.

If you enjoyed this write-up, please like and share. I don’t get paid to do this, so consider that my reward.

Also, if you have other ideas I should write about, my DM’s are always open on substack and Bluesky :)

All writeups are subject to our TOS

Amazing work as always

Any idea why this dumped 20% today ?