NFE Bond Update

RSA Out

For those that read my previous article, here is a quick follow-up.

Firstly, I would suggest reading through the following documents:

It's been about six weeks since I wrote up NFE and bought the 12% 2029s.

The RSA just dropped, and it's time for an update because the instrument I bought and the instrument I now own are not exactly the same thing anymore.

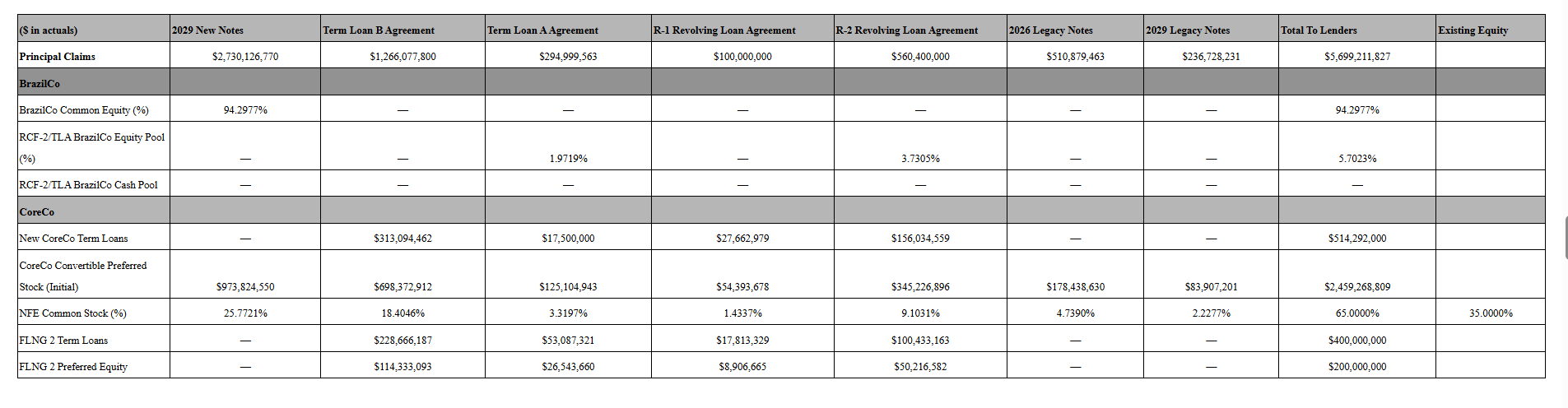

An abridged table of what is happening is below:

Disclaimer: I rushed this one out after reading through the 8-Ks and cleansing materials this morning, so forgive any errors and feel free to correct me in the comments.

In the original NFE write-up, the thesis was simple.

The 12% senior secured notes due 2029 (the "New 2029s") are the only rational place to sit in this capital structure because they had real Brazil collateral, structural seniority, and a believable recovery range anchored in hard asset EBITDA math.

The legacy 6.50% 2026s and 8.75% 2029s are lottery tickets that might get equity crumbs if the restructuring is generous, but you should not pay for that optionality.

That is what happened. Just more completely than I expected, and faster.

What NFE actually announced

Yesterday, NFE signed a Restructuring Support Agreement and outlined a UK Restructuring Plan (the “UK RP”) that separates the company into two independent pieces:

BrazilCo – a new, privately held entity owning the Brazilian terminals and power plants: Barcarena, CELBA, PortoCem, and the Santa Catarina/TGS terminal. Goes private. Owned by creditors. Managed by existing NFE management.

New NFE – a leaner, still-public company owning FLNG1 (the Liquefier, as Wes calls it), Puerto Rico/Genera, the Nicaragua terminal under development, and the remaining downstream assets.

On this morning’s call, Wes was direct about the scale of what happened:

“In the aggregate, NFE will have its corporate debt reduced from approximately $5.7 billion prior to this transaction to approximately $527 million. Obviously, a massive change in terms of the corporate structure.”

The RSA is already supported by more than 50% of existing creditors and more than 75% on the majority of the classes, with completion of the UK RP expected in 60–120 days, so mid-2026.

The 12.000% senior secured notes due 2029 were issued out of NFE Financing LLC in late 2024 as part of a ~$2.7 billion package to refinance near-term maturities.

They sat above Brazil via intercompany loans, paid 12%, and shared in a broader collateral pool that included meaningful Brazil exposure

Under the RSA those notes are cancelled as debt.

You get:

94.3% of BrazilCo equity – the residual ownership of a privately held Brazilian LNG-to-power platform sitting beneath the existing Brazilian project debt (BNDES term loan, Barcarena/PortoCem debentures, Brazil Financing Notes)

$974M face value of New NFE preferred – a three-year PIK instrument with a 3/5/7% step-up coupon (more on this below)

25.8% of New NFE common equity

The $2.5 billion of New NFE preferred equity is the key variable in this whole structure and it’s worth spending a minute on it because people are going to underestimate the conversion risk.

The terms, per Wes on the call:

Coupon: 3% in year one, steps up to 5% in year two and 7% in year three

These will be all PIK, no cash required from the company

Prepayment: fully prepayable at par at any time, no penalty

Maturity: three years, at which point any outstanding balance mandatorily converts into common stock

Conversion pool: converts into approximately 87% of New NFE common equity at maturity

So, bottom line, if the company does not refinance, your equity will be worthless after three years.

What is each entity worth

I think your best bet is to review the cleansing document and come to your own conclusions on how you value infrastructure businesses.

I usually use a 10x multiple, although a range of 5X to 20X is not unheard of depending on the stability and term of contracts.

Conclusion

If the Brazil business delivers, I am expected a par or greater recovery on the bonds on that alone based on the nature of the cashflows.

We are still waiting on the result of the Brazil power auction, so that is a risk which will be addressed in the next two weeks.

You also get a meaningful chunk of the newly delevered Core-co business with both an immediate common equity stake and converted (or later paid off) preferred equity as a sweetener.

Both businesses seem setup to succeed with much lower debt and stable cashflows.

If you have any questions, drop them in the comments and I will try to answer them.

If you enjoyed this write-up, please like and restack.

I don’t get paid to do this, so consider that my reward.

Substack seems to throttle free article writers, which makes attracting new readers difficult. I do not want to charge for this substack, but the algorithm may end up requiring it. I am trying to avoid this, so please spread this substack if you can.

Also, if you have other ideas I should write about, my DM’s are always open on substack and Bluesky :)

All writeups are subject to our TOS

I’m surprised no one has reported this and it has not been 8k’d, so maybe I get credit for the scoop.

$NFE New fortress Energy won multiple contracts at the Brazil power auction

CELBA won 2029 which is most likely the two power plants going online this year . At R$2.33 million/MW.year, that is over $800 million of revenue per year, if I’m doing my math right, so an over $12 billion dollar contract.

They can also potentially start the contract early with approval from the government or sell into the spot market if needed.

They also won the 2031 tender for a third expansion power plant, probably the 400 MW one they were working on.

https://agenciainfra.com/blog/lrcap-contrata-quase-19-gw-e-tem-100-empreendimentos-vencedores/

🥂🍾So far, so great. Plan makes sense to me.